A GST invoice is issued when a registered taxpayer offers taxable goods or services. Issuing and receiving GST-compliant invoices is a prerequisite for claiming ITC. If the taxpayer does not issue such an invoice to a customer who is a registered taxpayer, the customer will be disqualified from ITC and the taxpayer will lose the customer.

Who needs to issue a GST invoice?

If you are a GST-registered company, you will need to submit a GST invoice to your customers for the sale of goods and services.

What Are The Required Fields A GST Invoice Need To Have?

A tax bill is usually issued to rate the tax and by the skip at the enter tax credit. A GST Invoice should have the subsequent obligatory field-

Invoice wide variety and date

Customer name

Shipping and billing address

Customer and taxpayer`s GSTIN

Place of supply

HSN code/ SAC code

Item information i.e., description, quantity (wide variety), unit (meter, kg, etc.), the overall fee

A bill of supply is like a GST receipt aside from that bill of supply containing no assessment sum as the merchant can’t charge GST to the purchaser. A bill of supply is given in situations where expenses can’t be charged: An enrolled individual is selling absolved merchandise/administrations, The enlisted individual has decided on a synthesis plot.

Receipt cum-bill of supply

According to Notification No. 45/2017 – Central Tax dated thirteenth October 2017 If an enlisted individual is providing available as well as absolved products/administrations to an unregistered individual, then he can give a solitary “receipt cum-bill of supply” for every such stock.

Total Invoice

If the worth of various solicitations is not as much as Rs. 200 and the purchaser is unregistered, the merchant can give a total or mass receipt for the various solicitations consistently. For instance, you might have given 3 solicitations in a day of Rs.80, Rs.90, and Rs. 120. In such a case, you can give a solitary receipt, totaling Rs.290, to be called a total receipt

Switch Charge Invoice

A citizen responsible to pay a charge under Reverse Charge Mechanism (RCM) needs to give a receipt for labor and products or both got by him. The beneficiary will refer to the way that the assessment is paid under RCM. What’s more, they need to give an installment voucher while making an installment to the provider.

Debit and credit note

A debit note is given by the dealer when the sum payable by the purchaser to the vendor increments:

Tax receipt has a lower available worth than the sum that ought to have been charged

Tax receipt has lower charge esteem than the sum that ought to have been charged

A credit note is given by the merchant when the worth of the receipt diminishes:

Tax receipt has a higher available worth than the sum that ought to have been charged.

Tax receipt has higher duty esteem than the sum that ought to have been charged.

The purchaser discounts the merchandise to the provider.

Administrations are viewed as lacking.

What is the significance of GST receipt?

The significance of GST-consistent solicitations comes from the advantages they give out to the citizens. Here are the motivations behind why organizations ought to stay aware of the GST receipt design dominant during their exchanges.

Input Tax Credit implies asserting the credit of the GST paid on the acquisition of Goods and Services which are utilized for the assistance of the business. The Mechanism of Input Tax Credit is the foundation of GST and is one of the main explanations behind the presentation of GST.

As GST is a solitary assessment demanded across India (right from the production of merchandise/administrations till it arrives at the end client), the chain doesn’t become broken and everyone can take advantage of something similar and there is a consistent progression of credit.

For example-A broker buys a great worth Rs 100 and pays an expense of 10% on it. Furthermore, presently this broker-sold such products at Rs. 150 and gather a duty of Rs. 15 from the purchaser. Presently the merchant needs to pay Rs. 15 to the government however he had previously paid Rs. 10, so this Rs. 10 is ITC of the broker and will be permitted as an allowance from the charge payable and he needs to pay net Rs. 5 as assessment.

Fundamental Requisites/Conditions for Claiming Input Tax Credit (ITC)

The accompanying essentials are compulsory for asserting info tax reduction under GST

One should be enlisted under GST Law

A duty receipt or charge note was given by the enrolled provider showing the assessment sum

Labour and products have probably been gotten.

The provider ought to have recorded returns and paid such duty subsequently to the public authority.

Where products are gotten in parts or in portions, ITC is perhaps guaranteed on receipt of last parcel or portion.

Where information tax reduction is remembered for the expense of capital products and devaluation on such duty is asserted, no info tax break is permitted.

Input tax break won’t be permitted on the off chance that the equivalent has not been asserted inside the endorsed time limit.

How To Claim ITC

All customary citizens should report how much info charge credit (ITC) in their month-to-month GST returns of Form GSTR-3B. Table 4 requires the synopsis figure of qualified ITC, Ineligible ITC and ITC turned around during the duty time frame. The arrangement of Table 4 is given beneath: A citizen can guarantee ITC on a temporary premise in the GSTR-3B to a degree of 20% of the qualified ITC revealed by providers in the auto-produced GSTR-2A return.

Consequently, a citizen ought to cross-check the GSTR-2A figure before continuing to record GSTR-3B. A citizen might have asserted any measure of temporary ITC until 9 October 2019. Yet, the CBIC has informed that from 9 October 2019, a citizen can guarantee not over 20% of the qualified ITC accessible in the GSTR-2A as temporary ITC. This implies that how much ITC detailed in the GSTR-3B from 9 October 2019 will be complete of the genuine ITC in GSTR-2A and the temporary ITC being 20% of the real qualified ITC in the GSTR-2A. Thus, coordinating the buy register or cost record with the GSTR-2A becomes urgent.

People Who Are Allowed To Take Input Tax Credit

All enrolled individual is permitted to assume input charge praise other than the individual who is paying expense under the creative plot. An individual who has applied for enrollment somewhere around 30 days from the date on which he is responsible for enlistment is permitted to assume input charge acknowledgement regarding information sources held in stock and sources of info contained in semi-got done or completed products held in stock on the day promptly going before the date from which he becomes at risk to cover charge.

An individual who hast taken deliberately enrollment is permitted to assume input charge praise about information sources held in stock and information sources contained in semi-got done or completed products held in stock on the day promptly going before the date of award of enlistment.

An individual who has stopped to pay a charge under synthesis conspire is qualified to assume praise of information charge with data sources held in stock, inputs contained in semi-got done or completed merchandise held in stock, and on capital products on the day quickly going before the date from which he stops to pay a charge under arrangement plot.

Under the focuses 2, 3, and 4 over, the information tax break is permitted distinctly for the stock which is bought in the most recent one year from the previously mentioned date. Such individual necessities to document Form GST ITC-01 somewhere around 30 days of his becoming qualified for profiting input tax reduction. Subtleties outfitted in the structure are to be confirmed by a rehearsing contracted bookkeeper or cost bookkeeper if the information tax break guaranteed is more than Rs. 2 lakhs.

People Not Allowed To Take Input Tax Credit

People who are not enrolled in GST.

People who are enrolled under the synthesis plot.

Time Limit For Taking ITC

ITC isn’t permitted after any of the accompanyings occurs

due date of the return for September of next monetary year

yearly return petitioned for the pertinent year (Filing date, not due date).

As to rule 138 of the CGST (Central Items and Services Tax) Act, all firms registered under GST that transport goods valued more than Rs. 50,000/- must use the GST e-way bill or waybill. The E-Way bill is a compliance instrument that ensures that items are transported in compliance with GST laws. Prior to the transfer, it is submitted onto the GST portal with the appropriate information about the products being moved. This makes it easier to trace them.

What are the components of a GST E-Way Bill?

PART A and PART B are the two parts of the GST E-way bill that are generated.

Part A requires information from the person who is causing the movement of goods, such as his or her GSTIN (GST Number), delivery location (Pincode), invoice number (with date), the value of transported goods, HSN (Harmonized System of Nomenclature) code to classify the category of goods for calculating the tax slab, and the document number based on the mode of transport (Railway Receipt Number or Airway Bill Number or Bill of Lading Number, etc.), and

Transport information, such as transporter ID and vehicle information, is required in Part B. The transport information in Part B is used to generate the GST E-Way bill.

Benefits of GST E-Way Bills

The bill generation mechanism built under the VAT taxation system is no longer a bottleneck.

Different states set different regulations for creating E-Way Bills under the VAT system as well. There is a consistent and reliable mechanism for generating E-Way bills across the country under GST.

It provides a computerized interface for entering data and generating E-Way Bills, allowing for speedier goods movement.

It seeks to reduce the turnaround time, travel time, and expenses by being able to follow the movement of items.

Who needs GST E-Way Bill?

Consignor/Consignee: When a Consignor/Consignee registered under GST transports goods worth more than Rs 50,000, the appropriate individual is required to generate an E-Way Bill.

Transporter: The E-way Bill will be generated once the products have been assigned to the transporter to be transported.

Transporter by default: If neither the consignor nor the consignee has generated an E-way bill and the value of the items being transported exceeds Rs. 50,000/-, it will be the transporter’s responsibility to do so.

When a principal in one state/union territory transfers goods to a job worker in another state/union territory, the principal generates an E-Way Bill regardless of the consignment value.

Documents required to generate an E-Way Bill

The E-Way Bill portal (https://ewaybill.nic.in/) is where E-Way Bills are generated. Users log in and fill out the following documents with the required information:

For products carried, invoices, bills, and receipts are required.

Transport documentation – transporter ID and vehicle information (if items are transported by road).

Transport documentation – transporter ID, travel document number, and date (whether items are transported by air, sea, or land).

The validity of a GST E-Way Bill

The validity of an E-way bill is determined by the distance to be traveled.

The E-Way bill is valid for 1 day from the relevant date’ for distances less than 100 km.

The date on which the GST E-Way bill was generated is referred to as the relevant date.’

After the first 100 kilometers, an additional day is added to the existing 1-day E-Way bill validity, starting from the relevant date.

According to the principles of validity, this is not an extension, but rather an addition.

The validity period cannot be extended in most cases. Unless the commissioner issues a notification based on the type of goods.

In addition, if items are unable to be carried during the validity period, the transporter can alter the information in Part B of the FORM. GST EWB-01 and a new GST E-Way bill will be generated.

What are the penalties for non-compliance of the E-way bill system

According to Rule 138 of the Consumer Goods and Services Tax Act (CGST) 2017, if E-Way bills are not issued in compliance with the provisions of the CGST Rules, 2017, this will be regarded as a violation of the E-way bill system’s rules!

Taxable individuals who carry taxable products without the required documentation (including GST E-way bills) are liable to a penalty of Rs. 10,000/- or are considered tax evaders under the E-way bill system’s guidelines, according to Section 122. (Whichever is bigger at the time the application is submitted.)

Individuals who move goods or store them while in transit are in violation of the E-way bill system, according to Section 129 of the Consumer Goods and Services Tax Act (CGST) 2017. As a result, the products and documentation associated with them may be held or seized.

Transportation is an important part of the economy, as transportation issues disrupt the entire business channel. For this reason, changes in gasoline prices have a widespread impact on business disruption. The most popular form of goods transportation in India is road transportation. According to the Indian National Highway Authority, about 65% of freight and 80% of passenger transportation are carried by road. Transportation of goods on the road takes place from a transporter or courier agent.

Which goods transportation service is excluded from GST?

Goods transportation services are excluded:

On the road, except for the following services:

Goods transport;

home delivery trader

Through the inland waterway.

Therefore, the service of goods transportation by road remains tax-exempt under the GST system. GST applies only to the Goods and Services agency, GTA.

According to Notice No. 11/2017 Central Tax (Tax Rate) of June 28, 2017, the “goods transport agency” or GTA provides services related to the transportation of goods by road and provides consignment notes of any name. That is, other people can hire a vehicle for freight transportation, That is, others can hire vehicles to transport goods, but only those who issue consignment notes are considered GTA. Therefore, the consignment note is a mandatory requirement to be considered a GTA.

What is a consignment note?

A consignment note is a document issued by a forwarding agent against the receipt of goods for the purpose of transporting goods by road in freight transport. If the carrier does not issue a waybill, the service provider will not be part of the freight business.

If a consignment note is issued, this means that the goods Lien have been handed over to the carrier. The carrier is now responsible for the goods until they reach the recipient safely.

The consignment note is in sequence and includes

The Sender’s name

Recipient’s name

The Registration number for freight transportation where goods are transported

Product information

Place of origin-destination.

Person is liable to pay GST – shipper, consignee, or GTA.

What services does GTA offer?

This service includes not only the actual transportation of goods but also other intermediate/auxiliary services.

Load /unloads

Packing/unpacking

Trans-shipment

Intermediate storage, etc.

If these services are included and not offered as an independent activity, they also fall under the General Terms of Service.

What is the rate of GST on GTA?

Service by a GTA

GST rate

Carrying-agricultural produces milk, salt and food grain including flour, pulses, and rice organic manure newspaper or magazines registered with the Registrar of Newspapers relief materials meant for victims of natural or man-made disasters defence or military equipment

0%

Carrying- goods, where consideration charged for the transportation of goods on a consignment transported in a single carriage is less than Rs. 1,500

0%

Carrying- goods, where consideration charged for transportation of all such goods for a single consignee does not exceed Rs. 750

0%

Any other goods

5% No ITC OR 12% with ITC

Used household goods for personal use

0% **

Transporting goods of unregistered persons

Earlier exempted, but later made taxable; currently, list yet to be notified**

Transporting goods of unregistered casual taxable persons

Earlier exempted, but later made taxable; currently, list yet to be notified**

Transporting goods (GST paid by GTA)*

5% No ITC or 12% with ITC

Transporting goods of 7 specified recipients*

if GTA Charges 12%, GTA must deposit tax and ITC can be availed. Otherwise, if GTA, Charges 5%, RCM applies and the recipient must deposit tax and ITC cannot be availed

Hiring out a vehicle to a GTA

0%

According to the Notification 20/2017 Central Tax (Tax Rate) on August 22, 2017,

On December 31, 2018, the Government cancelled Notice No. 32/2017 Central Tax (tax rate) on October 13, 2017, and made purchases from unregistered dealers taxable. However, the list of registrants or transactions has not yet been communicated.

Is a GTA liable to register?

There was a lot of confusion as to whether GTA should be registered with GST. According to Central Tax Notice No. 5/2017 of June 19, 2017, GST-based registration is exempted for those who provide only taxable goods/services subject to the Reverse Charge Mechanism (RCM).

Therefore, GTA must register with GST if the consignee only ships goods for which the consignee is required to pay full tax (even if turnover exceeds the threshold) under the reverse charge basis. There is none.

Which businesses need to pay GST as part of GTA’s reverse charge?

The following businesses (recipients of the service) are required to pay GST with a reverse charge.

A factory registered under the Factory Act of 1948.

A society established under the Societies Registration Act of 1860 or any other law.

A cooperative is established under any laws.

GST registrant

A company established by law or under the law. Also

Incorporated or unincorporated partnership companies (including AOP)

Goods and Services Tax is an indirect form of taxation that greatly simplifies Indian tax law. GSTR4 serves as the GST return for compound dealers, a scheme offered under the GST scheme for certain categories of taxpayers. GST declarations for construction plans should now be submitted annually, but prior to 2018, they were submitted quarterly. In this article, we will take a look at compound dealer GST annual revenue, composition plan, and why it matters.

2. Things to Know About the GST Return for the Composition Scheme

3. Eligibility Criteria for the Composition Scheme under the GST regime

4. Composition Scheme under the GST Regime

5. GST returns for composition dealers

What Is GSTR4?

GSTR4 serves as a GST return for train dealers. Unlike regular taxpayers, who file up to three returns per month, parts dealers only need to file one return per year on the GSTR4 form only. Under normal circumstances, the last date to file a GST Competition Declaration is April 30 following the evaluation year. For example, taxpayers are required to submit their GST returns for the 2019-2020 composition plan by 30 April 2020. This year, however, the deadline has been extended due to the unexpected coronavirus pandemic. Under the GST scheme, all taxpayers who choose a layout plan must submit a GSTR4.

Things to Know About the GST Return for the Composition Scheme

1. The GST Portal now offers an offline Excel-based tool to help taxpayers file their GSTR4 annual reports on time. The ability to submit GST editorial declarations was added to the GST portal last August.

2. The GST filing deadline for construction plans has been extended from July 15, 2020, to August 31, 2020. This will be the new filing date for the GSTR4 report for the 2019-2020 tax year.

3. The deadline for submitting Form CMP02 to select how 2020-21 will be structured has been extended until June 30, 2020. This applies to registered taxpayers. Subject to both Section 10 of the CGST Act and anyone who has consented to the CGST Notice posted on March 7, 2019.

4. The ITC03 submission deadline has been extended to July 31, 2020, due to restrictions imposed due to the COVID-19 pandemic.

5. Taxpayers can file challans and CMP08 reports for Q1 2020 by July 7, 2020.

6. Taxpayers should be very careful when filing their annual GST reports for compound dealers. This is because they cannot be changed once submitted through the portal. Therefore, it is recommended that these dealers seek legal advice before filing a GSTR4.

7. Late submission of GST reports for compound dealers will incur a late fee of INR 200 per day prior to submission. However, the maximum fine that can be imposed is INR 5,000

Eligibility Criteria for the Composition Scheme under the GST Regime

Companies with an annual income of INR 1.5 million or more are eligible to apply for the constituent scheme. The threshold was originally set at INR 1 million per year, but CBIC later changed it to INR 1.5 million in 2019. Businesses should consider the revenues of all businesses using the same PAN card when calculating their total annual revenue. The government will consider gross sales when considering whether a business is suitable for a layout plan. In addition, only the following types of businesses can choose the configuration scheme in GST mode;

1. Manufacturers

2. Dealers

3. Restaurants that do not serve alcohol

The following individuals cannot opt for the Composition Scheme under the GST regime;

Composition Scheme under the GST Regime

Now let’s briefly review a few things to remember about Composition schemes

1. Complex dealers are required to pay taxes according to the reverse billing mechanism, where applicable. The shipping rate is the rate at which the dealer must pay tax on goods and services. Therefore, the tax rate under this scheme cannot be used to pay taxes under the reverse charge mechanism.

2. Composition dealers cannot avail of any input tax credit. Better known as ITC for the tax they paid under the reverse charge mechanism.

3. Such dealers do not have to pay the IGST since they have to pay only the CGST and SGST for the import of services or goods from an unregistered dealer under the reverse charge mechanism.

4. Complex dealers are required to pay a percentage of their total sales tax. And certain purchases are subject to tax according to the reverse charge mechanism. So total goods and services tax = supply tax + tax on B2B transactions (reverse charge) + tax on B2B purchases from unregistered dealers + tax on import services.

5. Unlike regular taxpayers, composition dealers do not have to keep detailed records of all financial transactions. Because the dealer pays the tax out of their pocket, you need to issue an invoice, not a tax invoice. These dealers cannot recover the GST paid to the customer.

GST Returns for Composition Dealers

Complex dealers are required to file the following declarations under the GST scheme:

1. Taxable individuals must pay tier taxes via a challan-cum-statement from 2019 onwards in the form of CMP-08.

2. From the assessment year 2019-2020, the frequency of filing GSTR4 has been changed from a quarterly to an annual basis.

3. GSTR-9A submissions continue to apply with some exceptions for the 2017-2018 and 2018-2019 evaluation years.

GST On Agricultural Sector : Most specialists accept that the effect of GST on the Agricultural area in India will be positive. In the general Indian GDP,

the agrarian business has a significant impact, being the significant supporter, covering practically 16%. Thus, the effect of GST on agribusiness should be concentrated widely to guarantee that ranchers don’t get the short finish of the straw.

The execution of GST could likewise assist with taking care of the issue of transportation of merchandise, laying out a National Market for rural products. Here is a more critical gander at horticultural items under GST, and the effect of GST on agribusiness in India.

What Is GST On Agricultural Sector Products

The Indian government has absolved GST on the horticultural business to a great extent. Basically, there is no GST on rural items like vegetables, produce, dairy, and new fish. Along these lines, all organizations that are a piece of the farming business, which don’t participate in handling don’t need to stress over GST.

Besides, organizations who exclusively supply labor and products are excluded from GST and can decide to quit enlisting for it. Thus, ranchers who sell their produce don’t need to pay GST on rural items. Moreover, seeds are likewise excluded from GST, helping make things more straightforward for ranchers.

Is GST Applicable On Ranchers?

According to the GST Act, ranchers are not responsible to pay any GST. Agriculturists who just stockpile items to others through developing their property don’t need to pay GST of any kind. They additionally don’t need to enlist for the GST. An agriculturist is any individual or HUF who develops their territory through;

Individual work

Work of family

Workers who help on paying wages in real money or kind

Recruited work under the oversight of any kind

Just small ranchers who follow this training are excluded from paying GST. Large organizations that work as an LLP, Company, or Firm which embraces cultivation should pay GST. In the event that they cross the standards for yearly turnover, they should enlist for GST and pay the expected obligation. Any person who does so is likewise permitted to benefit Input Tax Credit at whatever point material.

Impact Of GST On Agricultural Sectors

1. Agriculture is the foundation of our nation’s economy. The farming area contributes essentially to the nation’s creation. Truly, India is the world’s second-biggest maker of rural items. It represents around 16% of the Indian GDP. India moves a colossal amount of rural items like vegetables, organic products, tea, flavors, beats, and so on. This helps the public authority generally. In 2018-2019, the farming area contributed around 18% to the GDP of our country.

2. One of the serious issues in the rural area is that the ranchers can’t get the real incentive for their rural items. Likewise, the most difficult issue faced by the farming area is the transportation of horticultural items past the state limits all through India.

GST has to some degree settled the issue of transportation. By and by, there is no GST payable on the transportation of agrarian produce. GST is nearly giving India its first National Market for horticultural products. Preceding the execution of GST, when exchanges occurred on the highway, the yields were dependent upon different sorts of expenses. Additionally, there was a need to get a permit from every one of the states where the exchange was continued. This remained a significant downside in the exchange of cultivating items between states. In any case, after the execution of GST markets were changed for farming items.

3. Dairy cultivating, poultry cultivating, and stock rearing is uncommonly kept out of the meaning of Agriculture; henceforth these are responsible to be burdened under the GST system. The simple cutting of wood or grass, a get-together of leafy foods of artificial timberland or raising of seedlings or plants have additionally been explicitly kept out of the meaning of Agriculture, in this way these are likewise obligated to the GST.

4. Agri-wares like vegetables, organic products, milk, wheat, and rice are off 0 % charge. The expense on select milk items was charged at 2 %VAT; however, under the GST system, the price of new milk is nothing, and different items like dense milk and skimmed milk are charged at 18% and 5 percent separately. Dry natural products, jams, glue jams, and squeezes are accused of 12% and 18 percent. These rates are high contrasted with the 5 % charge prior.

5. A 12 % GST is forced on margarine and different fats (i.e., ghee, margarine oil, and so on) and oils got from milk; dairy spreads. Compost, which is a significant component of horticulture was recently charged at 6 %. Under the new GST system, the assessment on composts has been diminished to 5 %. A 12 % GST is required on manure-grade phosphoric corrosion. A GST rate of 18% is required on pesticides. GST likewise helps in diminishing the expense of large equipment utilized for delivering horticultural items. A GST of 18% is required on the assembling of farm haulers.

This is valuable in light of the fact that the makers are currently ready to guarantee the Input Tax Credit. The GST rate of 12% is pertinent to things similar to water siphons, draining machines, and self-dumping trailers and is utilized for horticultural purposes. Subsequently, assuming an agrarian purchases any of these items, he is responsible to pay GST as these items draw in GST

Positive Impact Of GST On the Agricultural Sector

The positive effect that GST has on the agrarian area has been examined as follows:

Upgraded the system of the store network

Credit for Input Tax

Transport time diminished

Tax Exemption

Ease intergovernmental exchange

Conclusion

An expansion in the expense of not many horticultural items is expected because of the increase in expansion for a concise period. However, execution of GST will help a great deal,

the ranchers/merchants over the long haul as there will be a solitary brought together public horticulture market. GST would guarantee that ranchers in India who contribute the most to GDP, will actually want to sell their produce at the best accessible cost.

There are 195 countries in the world, a majority of countries and territories border a sea or an ocean. These include almost all of the biggest countries which have territories on the 4 largest ocean basins – the Pacific Ocean, Atlantic sea,

Indian Ocean, and the Arctic Ocean. these have served as important zones for the movement of people, merchandise trade, shipping, and communication. The colonization of India by the Portuguese, French, and British happened by these sea routes. In the new age, this trade across oceans offers several advantages and also accrues tax repercussions. here, we deal exclusively with sales concluded over High Sea Sales and also assess their tax treatment under the Goods and Services Act.

1. Meaning of High Sea Sales

2. The legal status of HSS

3. How is a high sea sales agreement different from an import agreement?

4. Is there any limit on the number of times a high sea sales transaction can be concluded?

5. Documents required for an HSS transaction

6. High Sea Sales and therefore the Applicability of GST

In a regular overseas transaction, a buyer agrees to import a particular consignment of goods from another country. On this, tax is payable when the goods reach the buyer’s country. However, sometimes a buyer may sell his consignment to another person while it is still in transit, to a buyer in a 3rd country. Thus, goods do not physically reach the country of the real buyer and are re-routed midway.

This arrangement is also an HSS transaction. For e.g, a buyer in India contacts a jewellery merchant in the USA for importing jewellery to India. While this consignment is on the way, the Indian buyer sells this consignment to a buyer in Singapore. This is a high sea sales, without the goods or products reaching India. An essential requirement is that the agreement for high sea sales is signed after dispatch of goods or products from the origin and before they arrived at the destination.

The legal status of HSS

In a typical high sea sales transaction, more than 2 parties will involve. A person sending from the country of origin, the intermediate seller, and the final buyer of the goods or products. In a high sea sales transaction, it is the original consignee – who is named in the Bill of Lading who assigns the consignment in favour of another person.

This sale is concluded after the goods have left their port of loading in another country but before the goods or products have reached the port of discharge in India. on concluding the HSS agreement, the bill of lading should be endorsed in favour of the buyer or customer.

How is a high sea sales agreement different from an import agreement?

In the case of an import, the goods or products are physically received from the port of discharge and enter the domestic territory of the country. The person filling the Bill of Lading is the buyer of the goods or products and acknowledges his ownership over the goods. However, in an HSS transaction, the original importer assigns or sells the consignment to another buyer. Thus, unlike regular imports – goods don’t enter the territory of the country of the assignor.

The ownership of the goods or products also goes to the final buyer. Bringing goods into the country by way of import also attracts customs and GST, whereas these might not be applicable if the goods are directly sold while at sea to a buyer in a different country.

Is there any limit on the number of times a high sea sales transaction can be concluded?

No, there’s virtually no legal limitation on the times a high sea sales agreement may be done while the goods are still in transit. However, for each such sale concluded, GST will have to be paid.

Documents required for a high sea sales transaction

1. Commercial invoice

This is the sales invoice for the transaction. Such a commercial invoice under high sea sale must be within the local currency of the importing country, and not in foreign currency. This invoice must mention quantities of the items or things imported alongside their rates.

We provide the GST rate finder service. By using this service, you’ll be able to find the HSN code list with the GST rate. This finder service is also known as the HSN code The HSN code is used to find the GST rates of goods and services.

2. High Sea Sales Agreement

A high sea sales agreement is a written transaction between the high sea sales buyer and the high sea sales seller who finally receives the goods or products.

3. Consignee copy of Bill of Lading

A Bill of Lading is a very important document showing ownership and title over the goods or products. A consignee is a person who originally initiates the transaction from the country of origin of the goods or products. This copy of the bill of lading of the consignee is essential or important to demonstrate the passing of ownership of goods to a 3rd party on the high seas.

4. Certificate of Origin

This certificate provides information on the origin-destination of the goods or products. It serves many important purposes for calculating duties, certifying the quality, standards, etc that a country may have followed. You need to attach this certificate of origin form to the high sea sales invoice.

5. Import invoice

The import invoice reflects the original or initial agreement, concluded between the consignee and therefore the seller located in the initial country of export. This is different from the High Sea Sales invoice as the intermediate seller on high seas may alter the prices of the goods. It is essential to note that the import invoice will endorse by the high sea seller in favour of the buyer.

6. Insurance certificate

The original buyer of insurance for the goods or products for import may also assign the insurance in favour of the new buyer purchaser over high seas.

HSS and the Applicability of GST

Whether each successive transfer of goods Or products over high seas attracts GST

Until 2017, a lot of confusion prevailed over whether every time a sale takes place over high seas, GST would have to be paid. According to the rules under the GST and the Customs Tariffs Act, 1975, says the clarification by the Central Board of Excise and Customs. Imports will attract(IGST) only once when the import declarations file before the customs authorities for customs clearance purposes. Thus, only the goods or products will receive for the final time by the last importer who brings the goods into the Indian Territory, IGST can pay the final price of the item.

Scenario when IGST will need to be paid

Section 7 of the GST Act defines, a “supply” becomes taxable in India when goods enter the territory of India. just In case, the goods or products reach the domestic frontiers of India, after which the agreement with a seller concludes since the goods enter the borders. This supply becomes taxable, and [IGST] goods and service tax will have payment. Moreover, if the high sea sales conclude by an intermediary in India with a last or final buyer who is also in India, the final buyer would be liable to pay IGST.

The final or last buyer must have all important documents evidencing high sea sales. They’re the original import invoice, the high sea sales agreement, the new invoice. bill of lading, Bill of entry (required for customs clearance after the goods or products have reached India), certificate of origin, etc.

The availing input tax credit of IGST paid

Since the first or primary buyer of the goods or products pays no IGST or customs tax in India, there is no input credit on the tax. the final buyer or purchaser who pays IGST can avail of the advantage of the input tax credit. It is on the final price of the goods or products.

Given the different advantages in terms of taxation, saving of costs, fuel. Add. transportation, and time in concluding high sea sales, it’s an undeniably profitable trade. In recent clarifications by the tax, departments have highlighted that there would no tax liability. Tax liability accruing under [GST] Goods and service tax to the intermediary seller in a high sea sales transaction. Moreover, if the goods change hands multiple times throughout their transit, it is only the final or last importer. This brings the goods into the territory of India and would be liable to pay domestic taxes such as IGST.

According to the Goods and Service Act 2017, a replacement taxation scheme, i.e., the GST, is introduced to declutter the taxation regime and curb the cascading tax effect. Under the ‘One Nation One Tax’ initiative, the govt. of India (GOI) has extended a comprehensive and unified consumption tax scheme to exchange multiple indirect taxes on goods and services. GST could be a multistage tax because it is levied on various stages of production. But, it’s also a destination-based tax scheme which means all the taxes imposed on the assembly process are going to be refunded besides the ultimate customer. GST is often levied from the consumption point, not from the origin.

In India, there are 5 different tax slabs under the GST law: 0%, 5%, 12%, 18% and 28%. Since the GST scheme was introduced on July 01, 2017, by the 105th amendment, the first of July is well known as GST Day. there’s a GST Council consisting of finance ministers of the centre and also the states who take care of the tax rates and regulation of the GST. So with no further ado, let’s have a detailed observe the benefits and downsides of the GST.

Advantages of GST

1. Elimination of cascading tax effect

One of the foremost prominent benefits of GST is the unification of multiple taxes under an identical roof. It eliminates the many taxes on identical products and enhances the fluidity of tax processing. Let’s understand the cascading tax effect, i.e., the “tax on tax” effect within the pre and post-GST era with an example.

2. Enhanced threshold limit

In the Pre-GST era, businesses had to pay Value Added Tax after crossing the maximum limit of Rs. 5 Lakh. Again, the number varies from one state to a different one. However, after the implementation of GST, the edge amount has been increased by 15 Lakh, and also the new threshold limit is Rs. 20 Lakh. the rise within the VAT threshold limit has come as an enormous relief for tiny and medium businesses (SMBs).

3. Minimised compliances

Earlier, there have been separate compliances for every tax. as an example, if you had to file excise returns, it had been done monthly. the businesses and LLPs need to file service tax monthly, and partnership and proprietorship should file them quarterly. Similarly, the amount of filing the worth Added Taxes was also variable for various entities. However, with the GST coming into being, taxpayers have to file returns on just one occasion.

4. Using Composition Scheme Pay GST at fixed rates.

Did you recognize that the GST includes a provision for lowering the taxes for businesses? If your annual turnover is Rs.20 lakh and Rs.75 lakh, you’ll be able to go for the Composition Scheme to minimize your taxable income. The Composition Scheme allows you to pay GST at a hard and fast rate no matter your income if you fall within the bracket mentioned above of turnover. four basic conditions of the Composite Scheme:

The Composite Scheme is simply applicable to businesses dealing in goods, not services. However, restaurant owners can get the advantage of the scheme.

The scheme isn’t applicable to dealers who supply goods across the states and also not applicable to e-commerce dealers.

Dealers can’t collect Composite Tax from their clients or charge Input reduction (ITC).

The rates of Composite Tax are:

1% for traders

2% for manufacturers and

5% for restaurant owners

The Composite Tax Scheme has eased out the compliance burden and reduced the charge per unit, especially for the MSME businesses. it’s one of the foremost promising pros of GST.

5. Smooth and quick online processing

The big advantage of the new GST reign is the online filing of tax returns. you simply must visit the GST Portal, create your new account, log in, and begin filing GST returns. The interface of the portal is fairly smooth and easy. you’ll be able to file your GST on your own with basic knowledge of computers and therefore the internet. you’ll get all the main points regarding the GST jurisdictions, GST laws that you just need to fits, and every one the relevant information regarding filing the GST on the portal itself.

One of the most important beneficiaries of this new GST portal is startups. With the assistance of a web GST portal, it becomes easy to determine transparency among tax jurisdictions between State and Central governments.

6. Ease out the matter of warehousing for e-commerce and logistics companies

Before implementing GST, the logistic firms were accustomed to founding multiple warehouses within the state to waive off CST and state entry taxes. Moreover, because of the non-availability of a lot of products, the inventory was always below the optimum capacity in warehouses.

With the new GST regime in situ, logistics companies and e-commerce vendors can now find their warehouses at any location that suits their operability. it’s eliminated the unnecessary cost of warehousing for such businesses. The GST rule has also brought unorganized sectors like textile and construction under its umbrella and enhanced their accountability.

7. Takes e-commerce operators under consideration

Before GST regulations, e-commerce vendors weren’t explicitly defined under any law. They were charged variably under different taxation schemes. There was an excessive amount of confusion about these businesses as every state had separate provisions for e-commerce companies. In states like Rajasthan Kerala and West Bengal, e-commerce companies were treated as mediators and didn’t require paying VAT. In the province, they were treated as VAT compliant firms and registered their delivery vehicles for taxation.

With the new GST Scheme, these confusions are decluttered. The GST rules have defined e-commerce companies as separate entities and have extended specific provisions for them.

Disadvantages of GST

1. GST has increased the cost of operation

With the GST in place, businesses have to update their books and accounting with the latest GST-compliant software to keep their business afloat. ERP software is expensive, and it takes proper training to manage and run this software, thereby increasing the price to companies. Moreover, compliance with GST norms has drastically increased the operational cost of SMBs, they need to hire professionals to assist them out with the GST laws.

2. Tax liability Increased on SMBs

According to the prior scheme, the excise duty was levied only on businesses with an annual turnover of more than Rs.1.5 cr. However, now businesses with an annual turnover of more than Rs.40 lakhs must have to pay taxes under the new GST Scheme.

3. Enhance burden of compliance

Every company must register on the GST portal within the state of its operation. The entire process of registering, maintaining documents, invoices, and filing returns is tiresome. It unessential increased the burden on companies that had already been facing too many bureaucratic hurdles in India. On top of that, most states aren’t that savvy when it comes to technology, increasing the hurdles of compliances for the companies. All of these leads to enhanced difficulties for companies. especially for new businesses.

4. Penalties for non-GST-compliant firms

Every company has to register themselves with the GST portal, and if they don’t do so, they’ll have to pay penalties. It’s quite possible for MSMEs not to understand the nuances of the GST tax regime.

In GST (good service tax), the terms interstate and intrastate have tremendous significance within the determination of (Integrated Goods and Services Tax) IGST, (Central Goods and Services Tax) CGST, or (State Goods and Services Tax) SGST.

Interstate supply attracts (Integrated Goods and Services Tax) IGST, while intrastate supply attracts (Central Goods and Services Tax) CGST and (State Goods and Services Tax) SGST. during this text, we glance at the definition of interstate supply and intrastate supply as per the GST Act.

What is Interstate Supply?

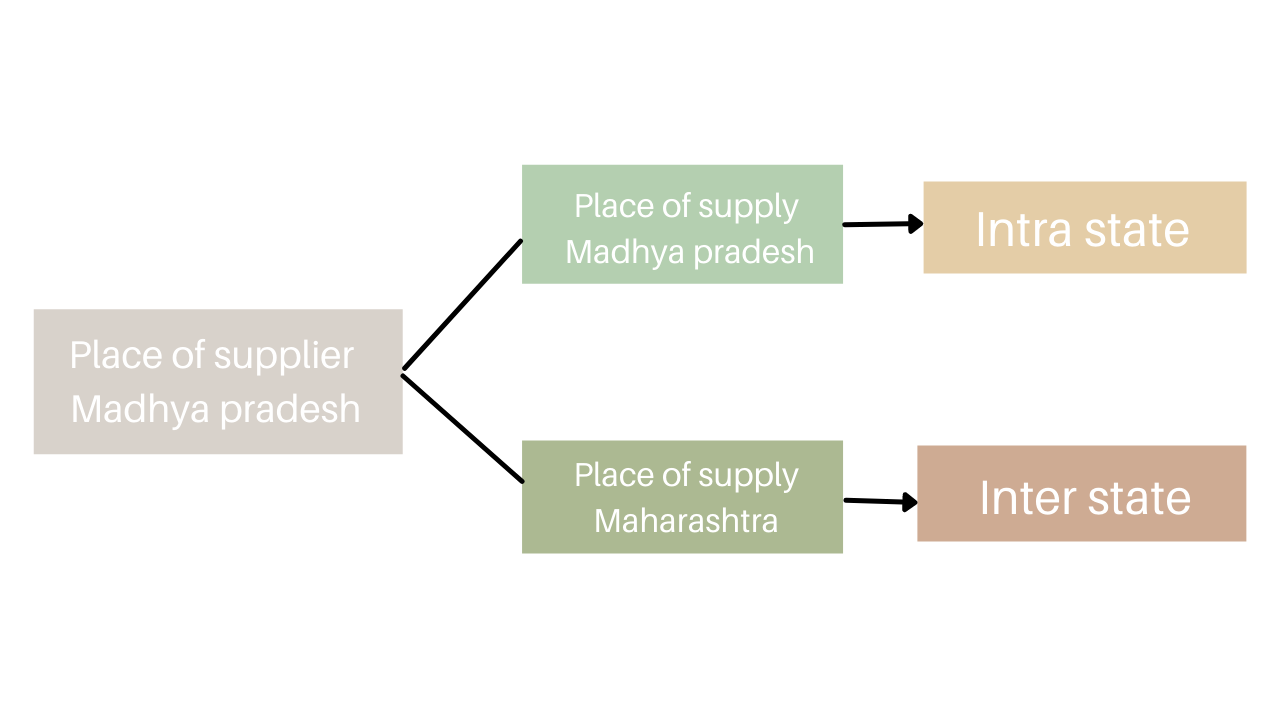

Under GST, the provision of products or services from one state to a singular would be called interstate supply. The GST Act defines interstate supply as when matters of the supplier and also the place of supply for the customer are in:

• Two different States; or

• Two different Union territories; or

• State and a Union territory.

The availability of products imported into India, till they cross the customs station is additionally classified as interstate supply. Under the interstate supply, one must pay only the IGST, and not CGST or SGST. The GST interstate also includes the supplies made by the SEZ (Special Economic Zone). The Integrated GST (IGST) would be charged on every taxable supply of products transaction & services provided on an interstate basis. it might even be supported by an identical price or value. Calculated in accordance with Section 15 of the CGST Law.

As per the GST Act, inter stat supply means the transportation of products or services between the state and union territory.

Before they reach the customs station, products delivered to India are frequently brought up as an Inter-State Supply.

Inter-State Supplies are the transportation of products and services from or to an exclusive economic zone or a selected development zone.

What is Intrastate Supply?

Under GST, the supply of products or services within the identical state or Union territory is termed an intrastate supply. However, the provision of products or services to a Special Economic Zone developer or Special Economic Zone unit situated within the identical state wouldn’t be an intrastate supply. Any supply of products or services to a Special Economic Zone developer or Special Economic Zone unit is classed as interstate supply.

The intrastate supply in GST is when the availability of products and services takes place within the state. Under this, the individual has got to pay both CGST and SGST. This doesn’t mean that there’s a rise in the tax. Rather, it’s capable of IGST and is simply divided equally within the name of CGST and SGST. within the intrastate supply in GST, both the supplier and buyer belong to the identical state.

Points To Recollect For Intra State Supply

A seller must collect both the State Goods and Services Tax (SGST) and therefore the Central Goods and Services Tax (CGST) from a buyer in Intra State Supply.

This stipulates that if the supplier’s and buyer’s positions are both located within the identical State, the provision is taken into account an Intra State Supply.

The Central Goods and Services Tax (CGST) is to be placed with the centralized, while the State Goods and Services Tax (SGST) is to be deposited with the authorities.

GST Interstate vs Intrastate Supply

The Integrated (GST)Goods and Services Tax, or IGST, is imposed on interstate supplies under the GST.

The GST rate for products and services sold within the state would stay unaffected.

The GST and rate, are going to be shared evenly between two headings: SGST and CGST.

Different taxes are charged on different commodities or services counting on the provision location under the present GST law.

If the transaction is an intra-state supply of products and services, the middle of Commerce collects the central GST (CGST), and also the State GST (SGST) is collected by the state where the provision takes place.

The Centre collects integrated GST on interstate supplies of products and services (IGST). during this instance, no CGST or SGST is applied.

The IGST rate is capable of the sum of the CGST and also the SGST.

Inter-state and intra-state supplies are laid out in Sections 7 and eight, respectively, of the IGST Act. Intra-state supplies occur when the supplier’s location and also the location of supply are both within the same state, while inter-state supplies occur after they are in separate states.

Example To Clarify The GST Interstate Vs Intrastate Supply Meaning

If an electronic store based in Bhopal, Madhya Pradesh sells an AC worth ₹1,20,000, to a different store in Pune, Maharashtra, they need to pay a tax of ₹21,600 as IGST. However, if the identical store sells the AC to a different store in Jabalpur, then they need to pay a tax of ₹10,800 as CGST and ₹10,800 as SGST, the overall amount remains identical.

this can be the simplest example for the intrastate supply in GST and interstate supply, and also the tax amount that needs to be paid.

Conclusion

The GST is one of the most effective tax reforms in Indian history, with several benefits within the short-term and long run. just in case you have got any issues calculating the GST amount, you’ll easily do so by using the GST calculator consistent with the tax rates and provide. Intrastate GST is imposed on the availability of products and services within one state or union territory, whereas interstate GST is imposed on the provision of products and services from one state to a different.

The GST is one of the foremost beneficial tax reforms in Indian history, with both short- and long-term rewards and disadvantages. GST interstate and GST intrastate concepts are important to see the applicability of IGST, SGST, and CGST. it’s important to grasp the supplier’s location and therefore the buyer’s location to work out whether the GST rate applicable is interstate or intrastate.

Goods and Services Tax (GST) in India dates back to the year 2000 and concludes in 2017 with four bills relating to it becoming an Act. The government designed to bring in an indirect tax regime with a theory of “ONE NATION, ONE TAX”. GST is a single tax on the supply of goods and services Under the GST regime, the tax is collected at every point of sale. In the case of intra-state sales, Central GST and State GST are charged. All the inter-state sales are chargeable to the Combined GST.

Objective of GST

· To attain the thought of ‘One Nation, One Tax’.

· To include a majority of the indirect taxes in India.

· To remove the falling effect of taxes.+

· To restraint tax dodging.

· To upsurge the taxpayer base.

What is GST returns

It is obligatory as per the GST Act, that every registered entity have to submit the details of their sales and purchases counting tax paid and collected on that by filing GST returns regularly. GST consultant team will handle this for our clients and let our clients focus on their business’s return is a certified document that provides all the purchases, sales, tax paid on purchases, and tax collected on sales-related facts. The GST returns are required to be filed, subsequent to which the taxpayer has to pay off the tax liability.

Disadvantages of GST

· Increased costs due to software obtaining

· Not being GST-compliant can involve penalties

· Smaller businesses will have a higher tax burden

· GST will mean an increase in working costs.

Types of GST

· Integrated Goods and Services Tax (IGST)

· State Goods and Services Tax (SGST)

· Central Goods and Services Tax (CGST)

· Union Territory Goods and Services Tax (UTGST)

Registration mandatory for whom

· Any business involved within the supply of products whose turnover in an exceedingly year exceeds Rs.40 lakhs for Normal Category states (Rs.20 lakhs for the Special Category States)

· Any business involved within the supply of services whose turnover during a year exceeds Rs.20 lakhs for Normal Category states (Rs.10 lakhs for the Special Category States)

· Every person who is registered under an earlier law (i.e., Excise, VAT, Service Tax, etc.) must register under GST, too.

· When a business that is registered has been transferred to someone/demerged, the transferee shall take registration with effect from the date of transfer.

· A person making inter-state supplies

· Casual taxable person

· Non-Resident taxable person

· Agents of a supplier

· Those paying tax under the reverse charge mechanism

· Input service distributor

· E-Commerce operator or aggregator*

· A person who supplies via e-commerce aggregator

· Person supplying online information and database access or retrieval (OIDAR) services from an area outside India to an individual in India, aside from a registered taxable person

Penalty for not registering under GST

An offender not paying tax or creating a brief payment must pay a penalty of 10% of the tax amount due subject to a minimum of Rs.10,000.

The penalty will at 100% of the tax amount payable when the offender has intentionally avoided paying taxes.

Document required

· PAN of the Applicant

· Aadhaar card

· Proof of business registration or Incorporation certificate

· Identity and Address proof of Promoters/Director with Photographs

· Address proof of the place of business

· Bank Account statement/Cancelled cheque

· Digital Signature

· Letter of Authorization/Board resolution for authorized signatory.